Access to financial services is a fundamental right, yet millions of people around the world remain excluded from the formal financial system. Financial inclusion is a critical step towards economic empowerment, allowing individuals and communities to save, invest, and protect themselves against financial shocks. Despite progress in recent years, many barriers still prevent people from accessing basic financial services, perpetuating cycles of poverty and inequality.

The Challenge

Sarah lives far from the city, in a small town surrounded by farms and dirt roads. She works at a nearby farm, earning a modest income in cash, and doesn’t have a bank account. Whenever she needs to buy electricity or mobile data, she walks to a small farm shop a few kilometers away. Despite her best efforts to hide her hard-earned money, she’s been robbed more than once, leaving her with barely enough to get by for the rest of the month. Her employer has encouraged her to open a bank account, but Sarah’s family has never had one, and the concept seems intimidating and unfamiliar. She longs for a secure and convenient way to manage her finances, but the idea of navigating the banking system daunts her.

Every few months, Sarah makes the trip to the city to stock up on items she can’t get in her town. During her latest visit, she decides to go to the bank and find out how to open a bank account. After waiting in line for hours, she finally reaches the front of the queue only to be met with the disheartening news: she must earn a minimum income to qualify for an account. Even if she could open an account, she’d be charged a monthly fee – an amount she cannot spare from her small salary. Disappointed and frustrated, she rushes to catch the taxi back to her town, returning yet again without access to the banking services she needs.

This is Sarah’s story, but it is also the story of many others in developing countries worldwide. Significant barriers such as transportation, requirements for a minimum income, monthly banking fees, and security concerns prevent people from gaining access to quality traditional banking services and becoming economically empowered. The vicious cycle continues and so the unbanked remain unbanked, excluded from the formal economy.

The Opportunity

WhatsApp banking and the concept of digital wallets can bring the previously unbanked into the financial sector by offering a comprehensive range of banking services within WhatsApp, a messaging channel that most are already familiar with and use daily.

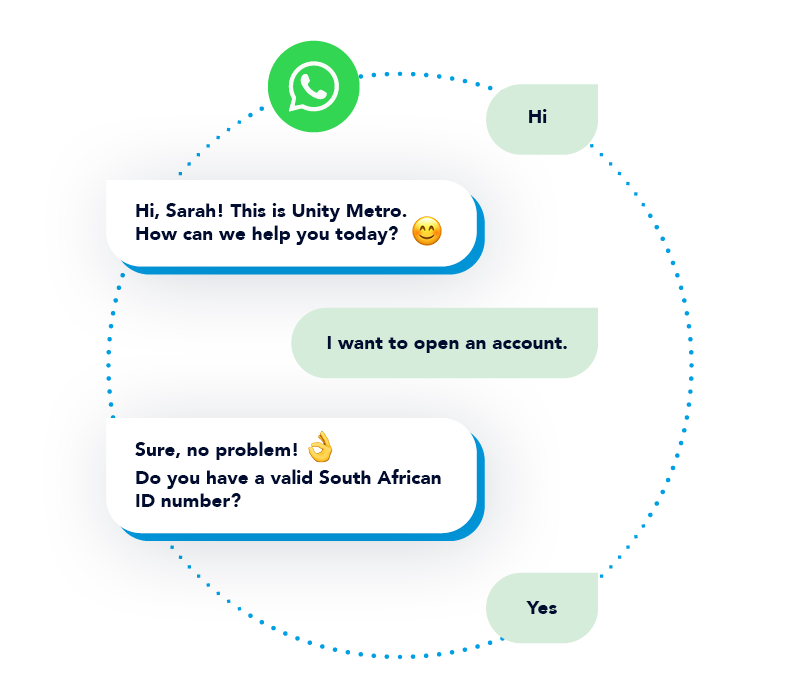

Possibly the biggest benefit of these digital wallets is the ability to open bank accounts remotely via WhatsApp, eliminating the need for customers to visit a physical branch or download additional apps that they must learn to use and which may consume significant amounts of data. Customers can simply chat to the bank, just like they would with family and friends. After following a few simple prompts and verifying their identity via checks with relevant government databases, they can open a bank account by taking a selfie and scanning a valid identity document. This removes a significant barrier to entry for those who previously had limited access to banking services due to living in rural areas or far from physical banks.

These digital wallet accounts can also be offered free of charge, i.e. no monthly banking fees, making it a much more appealing option for those who are already struggling to get by. With no minimum income requirements or other prerequisites, banking has become available to those who traditionally have been excluded.

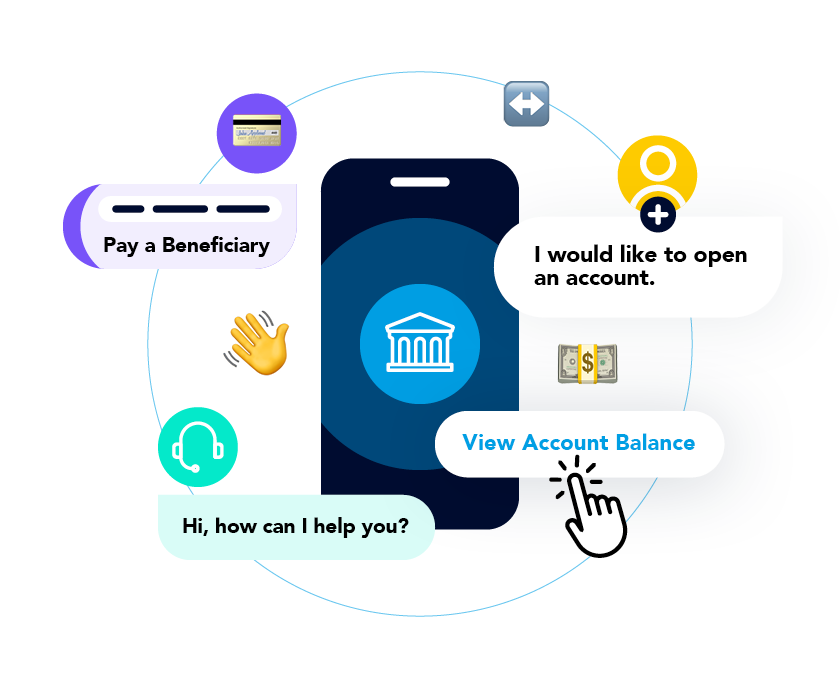

With digital wallets, making and receiving person-to-person payments and even settling utility bills is easy. Value-added services such as pre-paid electricity and airtime or data bundles are now quite literally at customers’ fingertips with little to no additional costs. Customers can receive money directly into their digital wallet, withdraw money, make payments, and recharge their wallet. Once onboarded, customers also get the opportunity to upgrade to even more comprehensive, robust, full function banking products, including things like debit orders, as the need arises.

Recent advancements in Artificial Intelligence (AI) and Natural Language Understanding (NLU) enables a more conversational approach to banking. Customers can interact with their bank in a more natural way, as you would with a person, as opposed to having to navigate complex menus and unfamiliar financial jargon. Using WhatsApp to request the bank to perform an action instead of merely answering questions, simplifies and speeds up transactions and makes it much less daunting for customers. What’s more is that banks can implement various authentication methods, from PINs to biometrics, to provide extra security and give customers a sense of control and peace of mind.

Bridging the Banking Gap

According to CGAP, financial inclusion means that all people and businesses have access to and are empowered to use affordable, responsible financial services (e.g., savings, credit, insurance, and payments) that meet their needs. Having access to these financial services improves their financial stability, increases economic opportunities, and reduces poverty and inequality.

WhatsApp banking presents a user-friendly, low-cost alternative that opens a wealth of opportunities ensuring everyone has access to quality banking services, regardless of their economic status or where they live. By removing some of the biggest barriers to inclusion in the financial sector, WhatsApp banking empowers people from all walks of life to take their finances into their own hands and break the cycle of the unbanked.

Step into the future of business messaging.

SMS and two-way channels, automation, call center integration, payments - do it all with Clickatell's Chat Commerce platform.